You do not own money, you hold a promise

Every headline about trillion-dollar deals, Federal Reserve rate decisions, or RBI interventions feels abstract. It is. But trace a single rupee from your wallet to a merchant's bank and the whole system reveals itself. This article is that trace — the honest mechanics of where money comes from, where it goes, and why the numbers in the news mean less than you think.

The money you hold is not what you think it is

Start with two words most people use interchangeably: currency and money. They are not the same thing, and the difference between them is the foundation of everything else in this article.

Money is an idea with three jobs. It stores value so you can save it. It exchanges for goods so you can trade it. It prices things so you can compare them. More than any of that, money is what makes it possible to do business with a stranger — someone you will never meet again, who has no reason to trust you, and whom you have no reason to trust. That is an extraordinary thing when you slow down to think about it.

Currency is the token that represents that idea. The note, the coin, the number in your bank app. Currency is the wrapper. Money is the trust inside it.

The distinction matters because the two can come apart. In Zimbabwe in 2008, the dollar was still a currency printed, numbered, and legally issued by the government. But it had stopped being money. Nobody believed it would be worth anything tomorrow, so nobody accepted it today. People switched to US dollars, South African rand, and sometimes barter. The token was still there. The trust had left.

Take a hundred-rupee note and look at it. Somewhere on it: "I promise to pay the bearer the sum of one hundred rupees," signed by the Governor of the Reserve Bank of India.

That sentence is the entire contract. The note is a liability of the RBI, not an asset. Before 1971, that claim could theoretically be traced back to gold. On August 15 of that year, Richard Nixon ended dollar-gold convertibility, and every major currency in the world became fiat money — backed not by a commodity but by government decree and collective belief.

Fact: The US dollar bill says "Federal Reserve Note" at the top. The Federal Reserve issues it as a liability on its balance sheet. The dollar in your pocket is, technically, a debt the US government owes you — redeemable for nothing except other dollars.

So what gives a rupee its value today? Mostly the belief of 1.4 billion people that it is worth something, backed by a legal mandate that it must be accepted for debts, and a reasonable expectation that it will not collapse by morning.

Trust is not soft. It is the load-bearing wall of the entire financial system.

Where money comes from before it reaches you

Most people imagine the RBI printing money, handing it to banks, and banks lending it out. That is roughly true for physical notes. But physical cash accounts for only a small fraction of the money in circulation. The vast majority exists as digital ledger entries, created by commercial banks when they make loans — not by any government printing press.

This process is called fractional reserve banking, and it is worth sitting with for a moment.

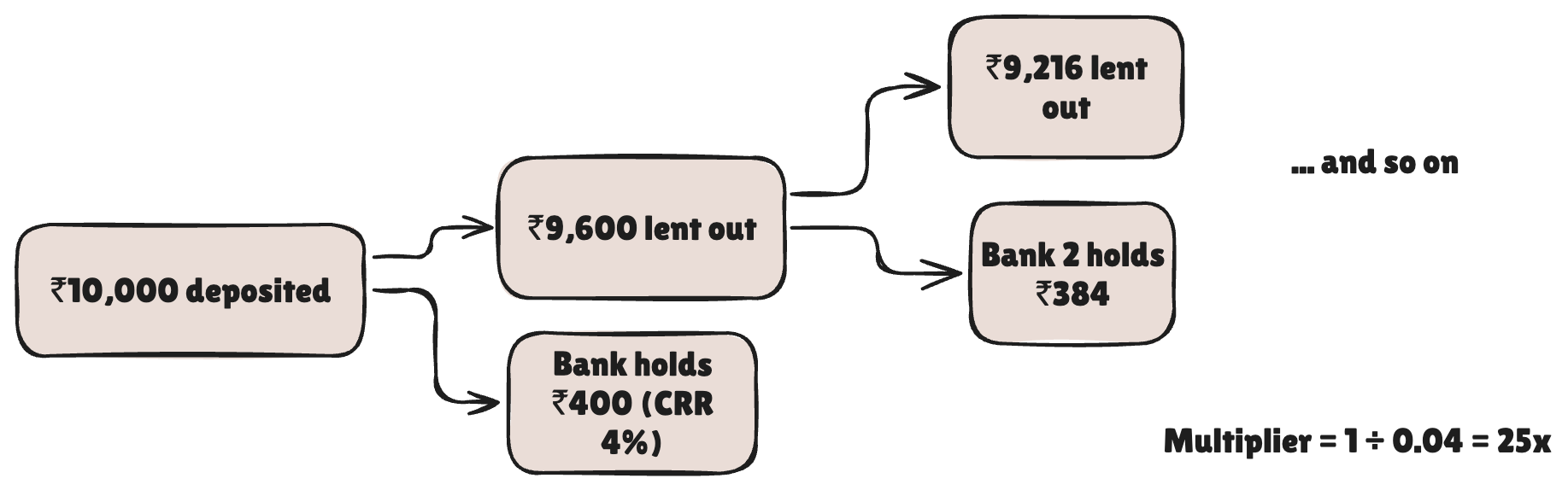

When you deposit ₹10,000, your bank does not lock it in a vault. It keeps a fraction in reserve and lends the rest out. The RBI mandates the minimum fraction through the Cash Reserve Ratio (CRR) — currently 4% in India. So for every ₹100 you deposit, your bank holds ₹4 and lends ₹96.

That ₹96 gets deposited somewhere else. That bank holds ₹3.84 and lends ₹92.16. Follow the chain to its mathematical limit, and you get the money multiplier: 1 divided by the reserve ratio. At 4%, the multiplier is 25. One rupee of base money can, in theory, support ₹25 in circulation.

Fact: India's broad money supply (M3) in early 2024 was approximately ₹210 lakh crore. Physical currency in circulation: roughly ₹35 lakh crore. The remaining ₹175 lakh crore exists purely as digital entries across bank balance sheets.

This is where inflation enters the picture. When banks create money through lending, more currency chases the same amount of goods and services. Prices rise. Your savings lose purchasing power quietly, with no announcement, no headline specifically addressed to you.

Inflation is usually described as rising prices. It is more accurately a fall in the value of money itself. The RBI targets 4% annually, which sounds modest — but at that rate, money loses roughly half its purchasing power in 18 years. The hundred rupees your parents saved in 2006 buys far less today. Moderate inflation is deliberate policy: it discourages hoarding, encourages spending, and keeps the economy moving. The problem is when it runs hot, as it did in India in 2022-23, when retail inflation crossed 7%, and ordinary people felt it most — their savings eroding faster than their wages rose.

Inflation is the cost of living in a fiat world. Understanding that is not pessimism. It is arithmetic.

The ledger journey of a single transaction

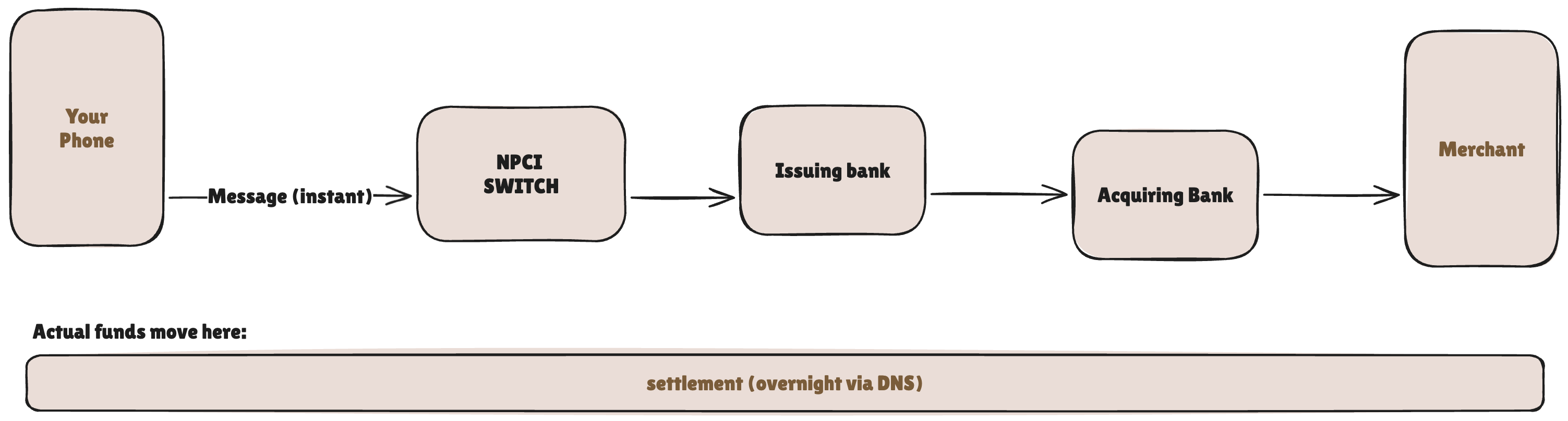

You are at a store. You tap your phone to pay ₹499 for a book. Three seconds. Here is what happens inside those three seconds.

Step 1: Your UPI app sends a payment request to your bank (the issuing bank) through NPCI's switch.

Step 2: Your bank checks your balance, verifies your UPI PIN hash, and authorizes the transaction in under a second through NPCI's IMPS infrastructure.

Step 3: The merchant's bank (the acquiring bank) receives confirmation that funds will arrive.

Step 4: Settlement. Here is where most people's mental model breaks down. What moved was a message. Not money. Actual settlement between banks happens through one of two systems:

- RTGS (Real Time Gross Settlement): For transactions above ₹2 lakh. Settled transaction by transaction, in real time.

- Deferred Net Settlement (DNS): For retail transactions. Banks accumulate everything throughout the day, net out what they owe each other, and settle the difference overnight.

Fact: NPCI processed over 14 billion UPI transactions in a single month in late 2023. The average transaction value was approximately ₹1,600. Most of those settled overnight in batch — not at the moment your screen said "Payment Successful."

The ₹499 that "left your account" instantly was a database update at your bank. The ₹499 that "arrived" at the merchant's bank was a database update there. The actual movement of settlement funds happened hours later, netting against thousands of other transactions running in parallel.

The rupee did not travel. Two databases were updated. And the only reason both parties accepted that update as real was the trust embedded in the system connecting them.

The invisible plumbing beneath every transfer

Scale this up to an international wire.

You send money to someone in the US. Your Indian bank almost certainly does not hold a direct account at their American bank — almost no two banks in different countries do. Instead, both routes through correspondent banks: large institutions like Citibank or JPMorgan that maintain relationships across the world on everyone else's behalf.

The accounts that make this possible have names. Nostro — from the Latin "ours with you" — is your bank's dollar account held abroad. Vostro — "yours with us" — is a foreign bank's account held at your bank. Most cross-border settlements run through this web of pre-funded accounts, with balances shifting rather than cash physically moving.

Here is something most articles skip entirely: the rupee is not freely convertible. It is a partially convertible currency, meaning the RBI controls how it moves across borders. India's forex reserves — around $640 billion — are held largely in US dollars, US Treasury bonds, and gold. When India conducts international trade, it predominantly settles in dollars. At today's rate of approximately ₹94 per dollar, that dependency is not trivial.

This is the legacy of the Bretton Woods system. After World War II, most major economies pegged their currencies to the US dollar, and the dollar alone was convertible to gold. Nixon ended that in 1971, but the dollar never lost its throne. It remained the world's reserve currency — the currency in which oil is priced, most trade is invoiced, and most central banks, including the RBI, hold their reserves.

In practice, the rupee is not backed by gold. It is backed by the dollar. And the dollar is backed by the full faith and credit of the United States government, which runs on its ability to collect taxes, issue debt, and maintain the world's continued trust that it will not default.

Fact: Approximately 58% of global foreign exchange reserves were held in US dollars as of 2023, down from 71% in 2000. Still dominant, but measurably declining.

SWIFT connects over 11,500 financial institutions across 200 countries and processes around 42 million messages daily. None of those messages moves money. They tell other systems to update ledgers. When Russia was cut off from SWIFT in 2022, it did not lose cash. It lost the ability to send and receive those instructions — which, in practice, amounts to the same thing.

What happens when the dollar's trust starts to crack

Most financial writing sidesteps this question. It should not, because the erosion is already visible and measurable.

The dollar's reserve status is not permanent. China and Russia have been accumulating gold and settling bilateral trade in yuan and rubles. India has signed rupee-denominated trade agreements with several countries, including Russia for oil. The BRICS bloc has discussed shared settlement mechanisms that bypass the dollar entirely.

Fact: Central banks globally bought more gold in 2022 and 2023 than in any year since 1967, led by China, India, Turkey, and Poland. This is not coincidence. It is systematic hedging.

A sudden collapse of dollar trust is unlikely. The sheer depth of US capital markets, the size of the economy, and the inertia of existing dollar-denominated contracts make rapid abandonment improbable. But a slow, multi-decade erosion — dollar reserves falling from 58% to 40% to 30% — is already underway.

What does that look like practically? More currencies settling trade directly without converting to dollars first. Gold and commodity-backed instruments regaining institutional relevance. Countries that built their reserves in dollar-denominated assets will face quiet losses as the dollar's structural premium fades — and India, holding most of its $640 billion in US treasuries and dollar positions, is not immune to that.

This is also where the large AI deals you see in headlines connect to the picture. When a sovereign wealth fund from the Gulf deploys $100 billion into US AI infrastructure, part of what it is doing is recycling petrodollars — oil revenue earned in dollars — back into dollar-denominated assets, reinforcing the very system that prices their oil in dollars. These circular flows are not accidental. They are the architecture of dollar dominance, running on autopilot.

A post-dollar world is not a collapsed world. It is a more multipolar one, where no single currency holds the structural advantage the dollar has held for 80 years. That transition will be slow, uneven, and politically messy. But knowing it is a direction — not just a theory — changes how you read the financial news.

How to stay grounded in a world built on debt and belief

Understanding all of this can feel disorienting. That is a reasonable response. The financial system is deliberately opaque — opacity benefits those who operate it. But opacity is not the same as chaos, and being unsettled is not the same as being in danger.

Here is what actually helps.

Know what you own. A savings account balance is a claim on a bank, not cash in a vault. A fixed deposit is a loan you made to the bank. Mutual fund units are claims on a pool of assets managed by someone else. Knowing the legal nature of what you hold is not paranoia — it is the baseline of financial literacy that most people skip.

Treat inflation as a fixed constraint, not a surprise. Money sitting idle in a low-yield savings account while inflation runs at 5-6% is a guaranteed, slow loss. That is not a forecast — it is how fiat systems are designed. Being intentional about where your savings sit is not about chasing returns. It is about not ignoring arithmetic.

Hold real things alongside paper claims. Gold, property, marketable skills — these have utility that survives ledger adjustments. Every central bank and sovereign wealth fund does this. It is not old-fashioned thinking. It is the same hedge that institutions making trillion-dollar decisions rely on.

Be deeply skeptical of anything that promises to beat the system. Guaranteed returns, leveraged trading platforms marketed to first-time investors, urgency-framed opportunities — these exploit exactly the anxiety that comes from not understanding how money works. The system is complex, but it is legible. Anyone claiming a loophole that regulators, banks, and institutional investors all somehow missed deserves your skepticism far more than your savings.

Spend 30 minutes a month reading primary sources. The RBI's monetary policy statements, NPCI's transaction data, the Union Budget's fiscal deficit numbers — all public, all free, all more useful than three months of financial news. Headlines are written to generate emotion. Source documents are written to record facts. The difference is worth your time.

Critical thinking is a financial skill. When you encounter a large number — a valuation, a deal size, a GDP figure — the first question is not "what does this mean for me?" It is: what is being measured, on what timeline, and who benefits from this framing? That habit, applied consistently, will protect you from more bad decisions than any specific investment strategy ever will.

Frequently asked questions

What is the difference between currency and money?

Currency is the physical or digital token — the note, coin, or bank balance. Money is the trust and value that token represents. A currency can exist without functioning as money, as Zimbabwe demonstrated in 2008 when its dollars became worthless despite being legally issued.

How does fractional reserve banking work in India?

When you deposit money, your bank keeps a fraction in reserve (the RBI mandates 4% as of 2024) and lends the rest. That lent money gets deposited elsewhere and lent again. One rupee of base money created by the RBI can support up to ₹25 in circulation through this chain.

What actually happens when you make a UPI payment?

Your UPI app sends a payment message through NPCI's switch to your issuing bank. The bank authorizes it, and the merchant's acquiring bank receives confirmation. What moved instantly was a message. The actual settlement of funds between banks happens overnight through batch processing called Deferred Net Settlement (DNS).

Why is the rupee backed by the US dollar?

After World War II, the Bretton Woods agreement pegged most major currencies to the US dollar, which was itself convertible to gold. Even after Nixon ended gold convertibility in 1971, the dollar retained its reserve currency status. India's forex reserves are held largely in dollars and US Treasury bonds, making the rupee indirectly backed by dollar trust.

What is SWIFT and why does it matter?

SWIFT is a global messaging network connecting over 11,500 financial institutions. It does not move money — it sends payment instructions between banks. When Russia was cut off from SWIFT in 2022, it lost the ability to send and receive those instructions, effectively blocking most international transactions.

What happens if the US dollar loses its reserve currency status?

A sudden collapse is unlikely. A slow erosion is already measurable — the dollar's share of global reserves has fallen from 71% in 2000 to 58% in 2023. A more multipolar world would mean more bilateral currency settlements, reduced dollar demand, and quiet losses for countries holding large dollar-denominated reserves, including India.

One rupee, fully accounted for

One rupee. Spent. Traced from its origins as a government liability to a UPI ledger update, from a Nostro account in New York to an overnight batch settlement, from the quiet arithmetic of inflation to the layered abstractions of billion-dollar AI announcements built on recycled petrodollars.

You now hold something that most people with strong opinions about the economy do not have: a working model of what is actually happening beneath the numbers.

The system is complex, yes. Politically influenced, sometimes unfair. The dollar's dominance is not permanent, and inflation is a real and ongoing cost. All of that is true, and none of it should be dismissed.

And the system still works. Transactions settle. Salaries clear. Loans get repaid, and houses get built. The architecture of money, for all its visible flaws, is functional — and it is legible to anyone willing to spend the time.

The people who navigate this world well are not the ones who panic at every headline or wave away every concern. They are the ones who understand enough to stay calm when others do not — who ask the right question instead of reacting to the loudest number, and who make decisions from a place of clarity rather than fear.

That is available to you now. Use it.

There is one more thing this article has not touched.

We have talked about how money works as a system. We have not talked about what money does to people — specifically, what happens when people start measuring themselves against each other with it.

In a society where net worth shows up in your car, your child's school, and the watch on your wrist, money stops being a medium of exchange. It becomes a scoreboard. And unlike the financial system, which at least has rules and institutions, the comparison game has no ceiling, no regulator, and no settlement window.

The rupee you just traced through ledgers and correspondent banks? It becomes something else entirely the moment your neighbour buys a new car with it.

That is a different kind of fiat system — and it deserves its own article.

Next: The scoreboard nobody designed but everyone plays